Archived Insight | January 5, 2022

This Q1 2022 multiemployer pension plan news recap covers:

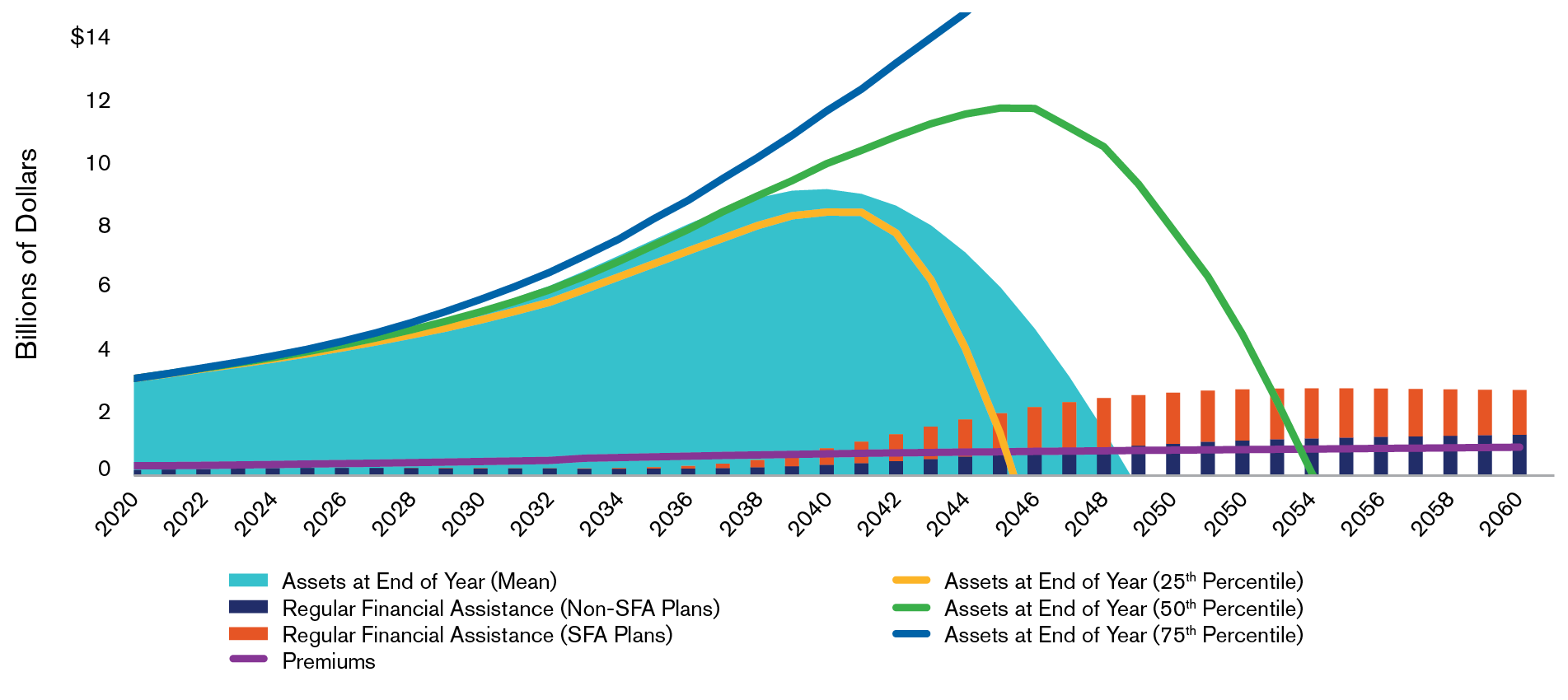

The following graph illustrates the wide range in the projected estimates of the solvency of the PBGC’s Multiemployer Program. The median projected year of insolvency is during the 2055 fiscal year, a significant improvement from last year’s projection of insolvency during the 2026 fiscal year. This improvement is due to the passage of the American Rescue Plan Act (ARPA) and the Special Financial Assistance (SFA) for financially troubled plans.

Source: PBGC 2020 Projections Report, 2021

Since 2000, passive investing has grown significantly in assets under management primarily due to attractive fees, exposure to a desired beta and retail investor appetite. However, fixed income is lagging in adoption relative to equities.

What is behind this difference in adoption? Equities are traded throughout the day through a centralized exchange, like the NYSE or Nasdaq, while bonds are over the counter instruments that trade much less frequently, making it difficult for as precise a valuation as more fungible publicly traded stocks. For bonds, this challenge for price certainty creates inefficiencies that active investors can capitalize on. Further, bonds are issued in a variety of ways, with different structures and characteristics in areas like convexity, maturity, capital structure position, optionality and duration. The median manager outperforms the Bloomberg Barclays Aggregate index over all trailing periods, while equity managers have had a much tougher time against the S&P 500. For more information, see Segal Marco Advisors’ September article.

The Segal Blend is a principles-based approach to valuing a pension fund’s unfunded vested benefits for withdrawal liability. The approach was developed by Segal actuaries and determines the liabilities using two different interest rate assumptions. Although commonly referred to as the “Segal Blend,” this method is not proprietary and many actuaries outside of Segal use this approach.

This need for valuing unfunded vested benefits came about after ERISA was amended in 1980 to address the dynamics of handling an employer withdrawing from an ongoing plan.

From its first challenge in 1983, there was a 35-year period free of any arbitration or court decision that rejected the use of the Segal Blend. This changed in 2018 when a district court rejected the use of the Segal Blend in the New York Times case.

Most recently, in September 2021, the Sixth Circuit Court of Appeals ruled in the Sofco case that the Segal Blend did not reflect the fund’s anticipated experience under the plan for purposes of calculating withdrawal liability. The ruling took a literal reading of the law, and did not allow the actuary to use assumptions based on the purpose of the measurement as directed by actuarial standards.

For now, it appears to be settled law for plans in the Sixth Circuit. However, the court noted that the PBGC is able to displace the court’s holding by releasing guidance on withdrawal liability assumptions. Learn more about the history of the Segal Blend and the Sofco decision in our October article.

Elections and relief are available under provisions of not related to SFA. These relief options bring back similar relief options from the Worker, Retiree, and Employer Recovery Act of 2008 and the Pension Relief Act of 2010. The elections allow plans to freeze their Pension Protection Act zone status, extend their current rehabilitation period or delay updating the plan’s funding improvement plan or rehabilitation plan.

Other funding relief provisions allow trustees to elect to modify the plan’s asset-smoothing method or spread certain investment losses and other experience losses related to COVID-19 over a longer period. See our October compliance insight for more information, deadlines and action items.

The IRS Employee Plans Compliance Resolution System allows plan sponsors to correct some mistakes under the Self Correction Program (SCP). For other types of mistakes, plan sponsors must submit an application to the Voluntary Compliance Program (VCP). This program was updated in Rev. Proc. 2021-30, released earlier this year. It includes the following changes:

For more information about these changes, see our July compliance insight.

Speak to our experts.

Start a Conversation

Health, Multiemployer Plans, Public Sector, Healthcare Industry, Higher Education, Architecture Engineering & Construction, Pharmaceutical, Corporate

Retirement, Investment, Multiemployer Plans, Public Sector, Consulting Innovation, Corporate

Retirement, Compliance, Multiemployer Plans, Healthcare Industry, Higher Education, Corporate, Communications

This page is for informational purposes only and does not constitute legal, tax or investment advice. You are encouraged to discuss the issues raised here with your legal, tax and other advisors before determining how the issues apply to your specific situations.

Don't miss out. Join 16,000 others who already get the latest insights from Segal.

© 2026 by The Segal Group, Inc.Terms & Conditions Privacy Policy Style Guide California Residents Sitemap Disclosure of Compensation Required Notices