Archived Insight | September 24, 2021

This Q3 2021 multiemployer pension plan news recap covers:

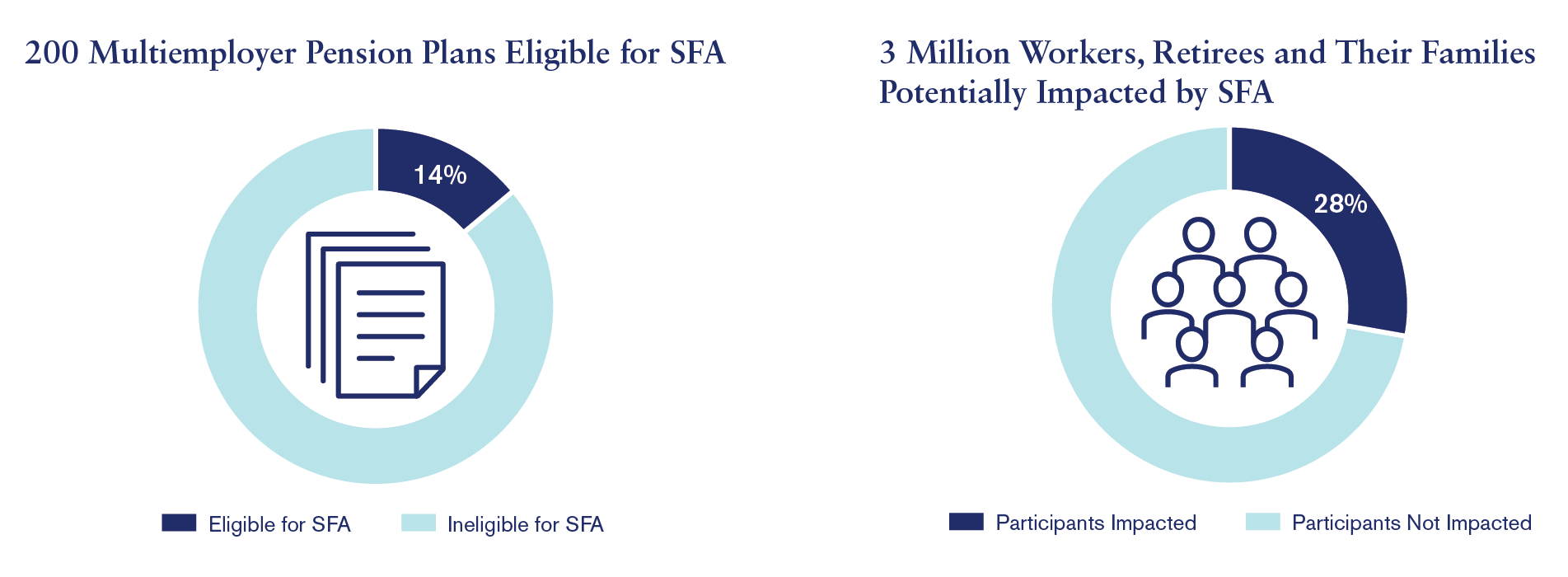

These are the key facts to know about ARPA and the special financial assistance (SFA) program:

Source: PBGC, 2021

Environmental issues are more prominent in the 2021 proxy season than in years past, matching an uptick in environmental focus seen in regulatory action and voluntary commitments coming from the private sector. New in 2021 are proposals centered on shareholder approval of climate-change plans. To date in 2021, 24 companies have put forth climate-change plans for shareholder approval. Segal Marco’s view is climate transition strategies are challenging to parse and not all shareholders have the expertise to evaluate the complexity. We are in favor of companies publicly disclosing their progress towards stated commitments.

See Segal Marco Advisors’ July 6 article for a more detailed discussion of environmental issues in the proxy season.

On June 21, 2021, U.S. Fed Chair Jerome Powell noted, “as these transitory supply effects abate, inflation is expected to drop back toward our longer-run goal.” What did he mean by that? Words are a highly imperfect representation of human insight, and human insight is — using some synonyms for “transitory” — ephemeral, fleeting and impermanent. Back in 2015, the Fed gave us insight into its so-called “forward guidance,” telling us that it provides communication to the public about the likely future course of policy.

It was John Maynard Keynes who said, “When the facts change, I change my mind — what do you do, sir?” This is how one should interpret the guidance we are now getting from the Fed: We don’t see permanent 70s-like inflation on the horizon based upon everything we know, but we do see stubborn unemployment. Given that we have had a long period of under-target inflation, we think we can stay accommodative with the expectation that inflation has some room to run while the U.S. economy returns to a more normal employment environment. We wouldn’t bet against that — for now.

Learn more about the Fed and interest rates in Segal Marco Advisors’ May 25 article.

ARPA, which was signed into law on March 11, 2021, created the SFA program under which the PBGC will provide grants to eligible plans that are facing insolvency.

Based on initial guidance from the PBGC, the multiemployer community must consider how this changes the landscape for troubled plans and the future of the PBGC, already itself under threat of insolvency.

Some SFA complexities to learn about and consider:

See our August 13 article for more information about ARPA’s impact on multiemployer pension plans.

The SECURE Act requires sponsors of DC plans with participant-directed investments to provide an individual benefit statement at least quarterly; other plans must provide the statement annually.

Under the current effective date, no notice is required until late 2021 or 2022; until the update is issued, it is not known whether this effective date will remain.

For plans with a recordkeeper, it is likely that entity will follow the new guidance. For plans without a recordkeeper, it will be important to take steps to ensure these lifetime income illustrations are set up properly. Segal can assist with these requirements.

The interim final rule contains required illustrations (single-life annuity, joint-and-100-percent-survivor annuity), required assumptions, model language, required timing of statements, and discussions of ERISA liability.

To learn more about the guidance on illustrating DC plan lifetime income, read our February 11 insight or consult your Segal consultant.

The IRS has extended, for an additional year, its temporary option to use e-signatures and video for any participant elections that a plan representative or a notary public must physically witness. This pertains to obtaining spousal consent to waive optional benefit forms. The latest IRS guidance extends the relief, without change, to June 30, 2022.

For more information about this “physical presence” relief, see our June 28 insight.

Speak to our experts.

Start a Conversation

This page is for informational purposes only and does not constitute legal, tax or investment advice. You are encouraged to discuss the issues raised here with your legal, tax and other advisors before determining how the issues apply to your specific situations.