Articles | August 4, 2022

Pension risk transfers (PRTs) have become an increasingly popular tool for organizations that are looking to reduce the long-term financial obligations and risks associated with their DB pension plans.

This article discusses a specific type of PRT strategy: an annuity buyout. It covers the factors organizations need to consider before deciding whether to pursue this risk-mitigation strategy.

Share this page

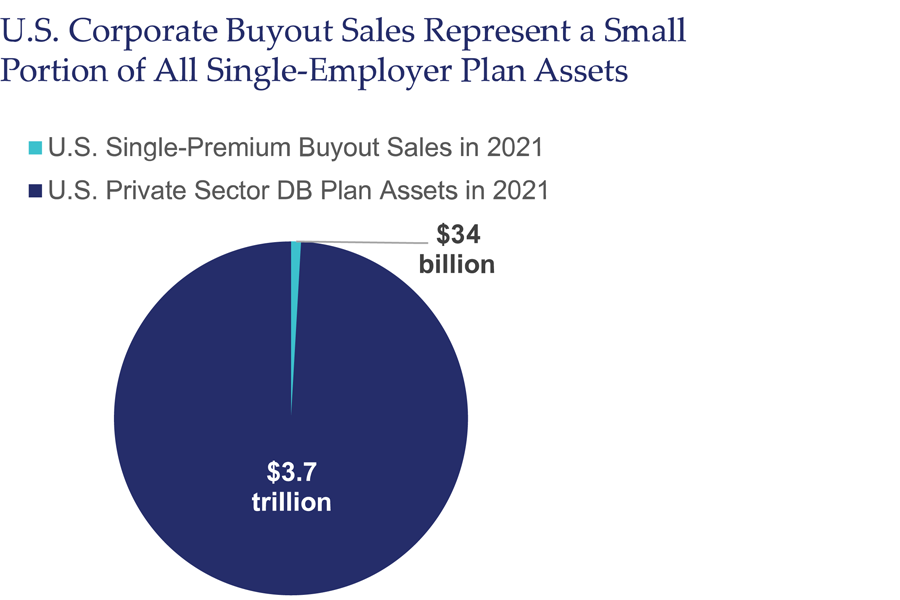

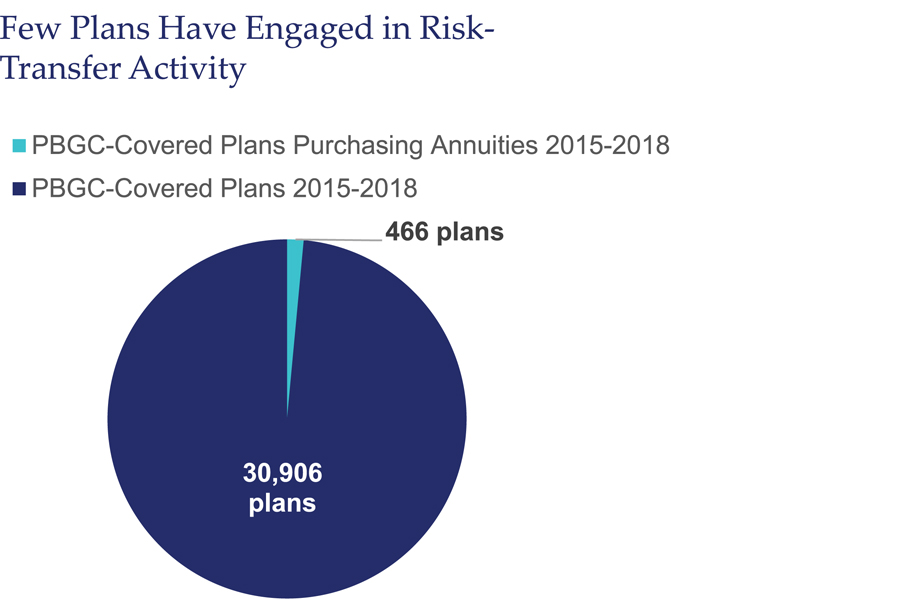

An annuity buyout involves purchasing a group annuity contract with an insurance company in exchange for taking over all future benefit payment obligations for the affected participants. In 2021, approximately $34 billion of U.S. DB plan assets were sold through an annuity buyout. While this may seem like a large number, it represents less than 1 percent of all private sector DB plan assets. Further, a recent PBGC study on risk transfer activity for the period 2015 through 2018 showed that less than 2 percent of all single-employer DB plans have engaged in a risk-transfer activity.

Although these transactions can be beneficial, there are many factors to weigh when considering this specific risk-mitigation strategy.

The cost of transferring participant liabilities to an insurance company may result in a significant reduction in the plan’s funded status for the remaining pension liabilities in the plan. This reduction in funded status will cause an increase in the plan’s minimum funding requirements in the years immediately following the risk transfer.

The reason for this is that while insurance companies measure pension liability on an economic basis, for IRS minimum funding calculations, the liability reflects a much longer-term average of corporate bond rates. This difference in measurement will result in a greater reduction in plan assets (used to pay the insurance premium) than reduction in plan liabilities on an IRS minimum funding basis.

PBGC premiums are an unavoidable cost to all qualified DB plans. Pension risk transfers are often viewed as a strategy to help reduce these expenses. Here’s why: every participant removed through a risk transfer leads to immediate savings in the flat-rate premium ($88 per participant in single-employer plans for 2022).

However, the impact on the plan’s variable-rate premium (VRP) is not as straightforward. On the positive side, if a plan’s VRP is limited by the per-participant cap ($598 per participant in single-employer plans for 2022), each participant removed from the plan will lead to a direct savings. Conversely, if a plan’s VRP is not at the per-participant cap, the impact of an annuity purchase could result in an increase in VRP based on the change in funded status. Once again, this is due to the amount of assets leaving the plan exceeding the corresponding liability. (Note that the liability measured on a PBGC basis will be closer to the insurance premium than the IRS funding liability but will still likely be less).

The example below compares two plans that engaged in an annuity purchase for a subset of their retiree population. In both cases, the plan moves 100 retirees out of the plan to an insurance carrier, resulting in a $1,000,000 decrease in PBGC liability and a $1,250,000 decrease in assets. The example demonstrates how two plans with the same starting liability and the same annuity purchase price can have significantly different outcomes with regard to PBGC premiums.

Plan A’s VRP premium is below the per-participant cap prior to the annuity purchase and the cost of the sale causes the VRP to increase. Plan B, however, is above the per-participant cap and sees significant VRP savings.

When estimating potential premium savings for future years, plan sponsors should not only consider if their plan is currently at the per-participant cap, but also how far into the future the plan is projected to stay at the cap.

Accounting implications also need to be considered when determining if an annuity buyout makes sense. Although accounting interest rate assumptions tend to be closer to those used by insurance companies, the economic liability in an annuity purchase could still be higher which would lead to a greater reduction in assets than liabilities on the balance sheet (though not nearly as significant as the funding liability impact).

Further, under U.S. GAAP accounting rules, if the reduction in benefit obligation from a buyout is greater than the plan’s service cost plus its interest cost, a settlement charge must be recognized. This will require a percentage of any outstanding losses to be immediately recognized in the current year’s pension expense. To avoid this, plan sponsors will sometimes choose a specific subset of their population to include in the annuity purchase to ensure that the final premium paid to the insurance carrier is below the settlement threshold.

If a plan falls below an 80 percent funded status on an IRS funding basis, benefit restrictions are enforced on certain plan payments and the ability to use the plan’s credit balance is temporarily revoked.

As mentioned above, the impact of an annuity buyout on a plan’s funded status could be significant. In some cases, it could push the plan below the 80 percent threshold. To avoid this, plan sponsors may choose to use cash to fund the plan up to a desired level that will avoid any unintended consequences post transaction. (Clearly, the ability to fund this cost is an important consideration.)

Although most plan considerations are of a financial nature, plan sponsors also need to consider how their decision might affect plan participants.

While an annuity purchase does not change the benefit amount participants will receive, it does remove the insurance protection that the PBGC provides for the continuation of those benefits. Most states do not guarantee the same level of coverage that the PBGC guarantees.

Moreover, insurance companies do not protect pensions from creditors. Insurance companies can choose how to allocate their reserves and unlike qualified DB plans, they do not need to annually disclose this information to participants.

Plan sponsors should be prepared to create a smooth transition for transferred participants by delivering clear messaging about the reason for the transfer and allocating increased support resources.

After making the decision to engage in an annuity purchase, plan sponsors and fiduciaries have additional decisions to make. During the process of choosing an insurance provider for an annuity purchase, risk advisors may have pre-established relationships with specific insurance companies. Under ERISA Law, fiduciaries are required to make decisions in the best interest of all participants.

To oversee all advisors and make sure they are working together to choose the best strategy, as well as select the right provider and receive the best price possible, it can be helpful to retain a consultant.

As shown in the chart below, there are several positive reasons for a plan sponsor to engage in an annuity buyout. But there are also several negative outcomes that could arise depending on your plan’s specific economic situation.

PRTs are not a one-size-fits-all solution. Plan sponsors should conduct a thorough analysis of the possible outcomes before embarking on this path.

While reducing your plan’s risk exposure is usually a prudent decision, there could be other risk-mitigation strategies that suit your organization’s risk goals better than a PRT.

A liability-driven investment (LDI) strategy is a common way plan sponsors address funded status risk, which does not remove liability from the plan but instead focuses on investing plan assets to generate returns that are positively correlated to the plan’s liability return. One example of this type of strategy is to invest in a bond portfolio whose value will change in conjunction with changes in discount rate (i.e., as liabilities move up or down due to discount rate changes, the corresponding asset portfolio for those liabilities will move in lockstep).

Plan sponsors may also wish to focus on the design of their retirement offering to active employees as a way of reducing cost volatility. While an annuity purchase may be ideal for plans that have a large retiree population, plans that have many active employees who are still accruing benefits may want to consider replacing future accruals in the pension plan with a comparable benefit from a 401(k) or 403(b) plan. Such plans can be designed to provide a similar level of retirement benefit as the pension plan, while avoiding large swings in employer cost each year.

Retirement

Retirement, Compliance, Multiemployer Plans, Public Sector, Healthcare Industry, Higher Education, Architecture Engineering & Construction, Corporate

Retirement, Compliance, Multiemployer Plans, Public Sector, Healthcare Industry, Higher Education, Architecture Engineering & Construction, Corporate

This page is for informational purposes only and does not constitute legal, tax or investment advice. You are encouraged to discuss the issues raised here with your legal, tax and other advisors before determining how the issues apply to your specific situations.

© 2024 by The Segal Group, Inc.Terms & Conditions Privacy Policy California Residents Sitemap Disclosure of Compensation Required Notices

We use cookies to collect information about how you use segalco.com.

We use this information to make the website work as well as possible and improve our offering to you.